“Mobile money” refers to mobile-based money transfer and savings services. Mobile money has been around in Kenya about 10 years, and according to CCN, the biggest brand, M-Pesa, has 18 million active users in the country and has lifted 2% of Kenyan households out of extreme poverty. Proponents of mobile money explain this by mobile money enabling safer and easier savings, and reducing financial barriers and transaction costs to starting a small business. A competitor was interested in seeing how it could increase its market share.

The client conducted a survey about 399 individuals’ mobile phone and mobile money use. I was also provided with access to a snapshot of the same individuals’ mobile money transaction data. (I describe my approach to the data analysis below but if you’d like to skip to the presentation of my findings, here it is).

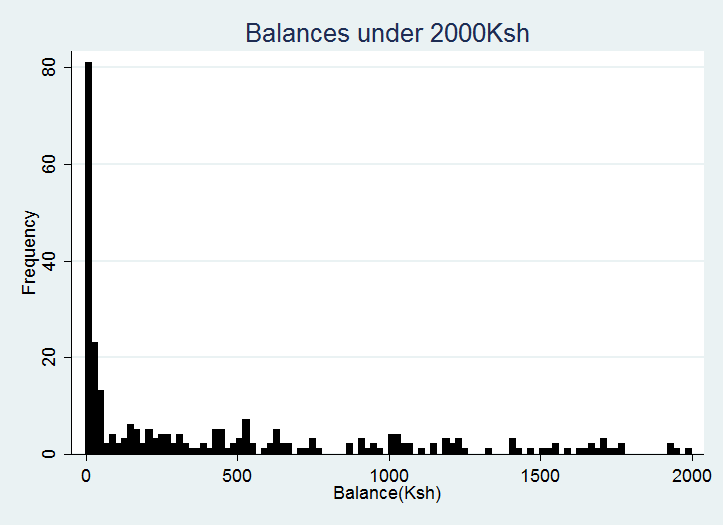

The data required considerable cleaning for removal of duplicates and correction of typos. I then visualised the transaction data. One of the most interesting things I found as I was exploring was that the balance on the mobile money accounts seemed highly skewed towards low balances.

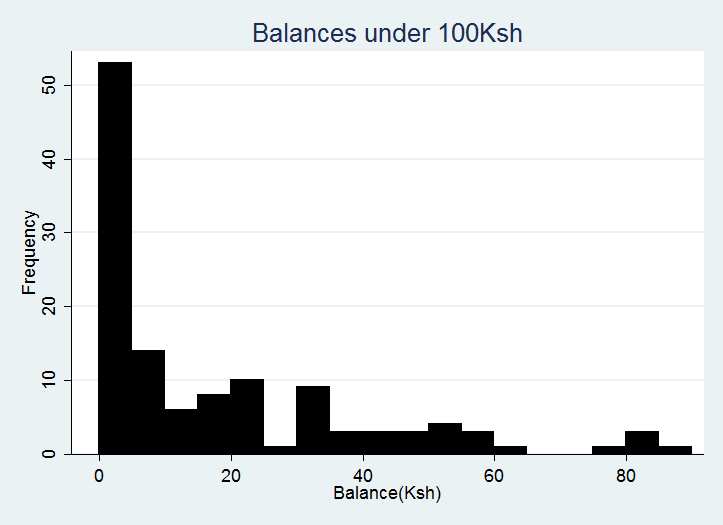

So I zoomed in a bit…

These graphs gave initial indications that these particular customers don’t seem to use the mobile money accounts for long-term savings (the modal value of savings is 0-5 Kenyan Shillings (about US$0.05)). The below graphs which show the deposits being low relative to receipts of money also suggest that the accounts are being used more to enable transactions than savings.

I linked the transaction data with the survey data to understand who the customers were, and their behaviour with regard to mobile phone and mobile money use. I used OLS regression (with accompanying tests) to model the costs associated with mobile money, and probits to model the probability of choosing a provider, of using their mobile money service and of starting using it within the last year. I then hypothesised about the behavioural barriers to accessing the client’s mobile money services, and created some recommendations on the findings.

I was most interested to find that customers perceive that comparing prices between providers, switching providers and sending money to another network is difficult. The customers were very familiar with the price of sending money, weren’t convinced to change networks by promotions and the most frequently chose a provider because they trusted them. Because of the lack of responsiveness to promotions, I advised the client to focus on developing products which were relatively expensive or under-provided in the current market.

Please see the presentation of my findings.